Some African states are not merely "challenged." They are structurally incentivised to underperform. Until that incentive structure changes, reforms will remain cosmetic.

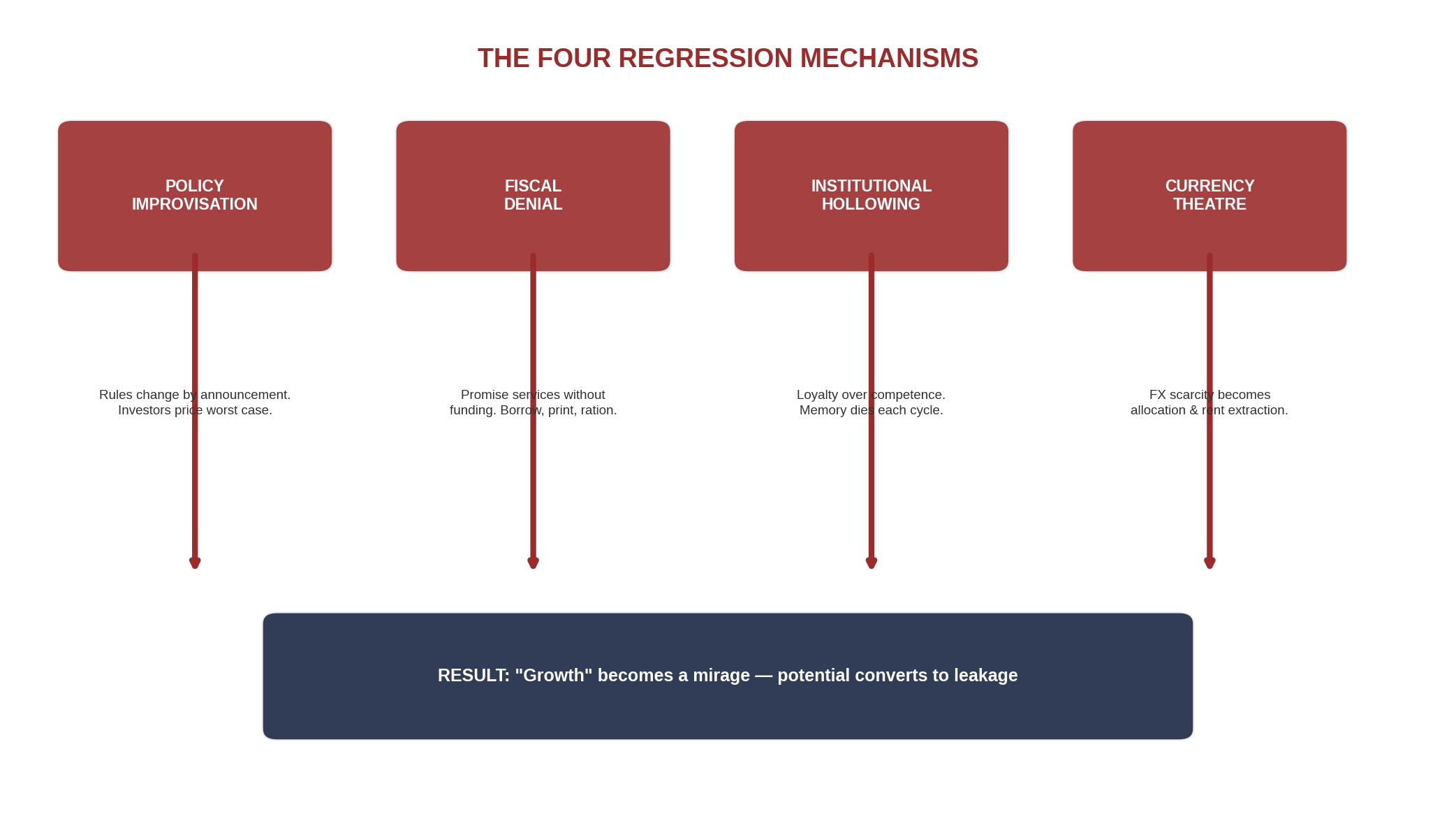

The Regression Mechanism

Regression shows up through four mechanisms:

The four mechanisms that convert potential into leakage.

Policy Improvisation: Rules change by announcement rather than process. Investors price the worst case—because it arrives often enough to be rational.

Fiscal Denial: States promise services without funding them. The gap is financed via debt, monetary expansion, arrears, or distortions.

Institutional Hollowing: Competence is treated as politically dangerous. Loyalty is safer than ability. Institutional memory dies.

Currency Theatre: Foreign exchange scarcity becomes an administrative allocation problem—creating an ecosystem of rationing, discretion, and rent extraction.

When these four combine, "growth" becomes a mirage—because the state has built a machine that converts potential into leakage.

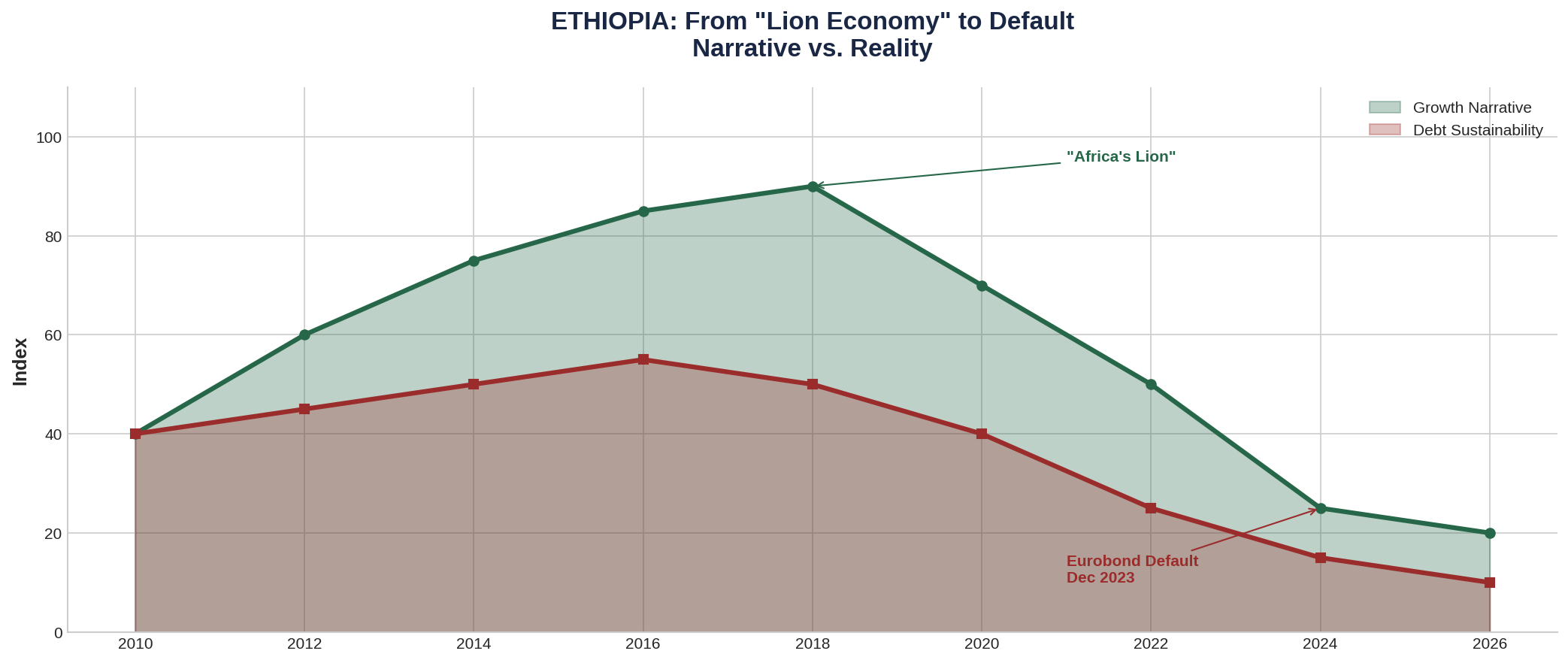

Ethiopia: The Arc from Lion to Default

Ethiopia's trajectory: from "Africa's Lion Economy" to Eurobond default.

Ethiopia was Africa's investment darling for a decade: state-led industrialisation, 9 per cent growth, manufacturing ambition. The Grand Ethiopian Renaissance Dam, completed in 2025 after fourteen years, stands as Africa's largest hydroelectric project—financed almost entirely through domestic bond issuances and salary contributions from public-sector workers. The achievement is real.

So is the debt crisis. Ethiopia entered the G20 Common Framework for debt restructuring in 2021. In December 2023, it defaulted on its $1 billion Eurobond—the first African sovereign to default on international bonds since Ghana. As of January 2026, the restructuring remains incomplete: official creditors signed a Memorandum of Understanding in July 2025, but private bondholders rejected terms in January 2026 after the Official Creditor Committee ruled that proposed Eurobond treatment violated "comparability" principles.

Fitch assigns Ethiopia a "Restricted Default" rating. The IMF's $3.4 billion Extended Credit Facility, approved in July 2024, is contingent on debt relief that has not yet materialised. For investors, Ethiopia is now a restructuring story—not a growth story.

The lesson is not that Ethiopia is uninvestable. It is that growth narratives cannot substitute for debt sustainability. A country can build a dam and still default on its bonds.

Nigeria: Scale Without Coordination

Nigeria's regression is more chronic than acute. The economy has not collapsed; it has underperformed its potential for two decades.

In 2024, the national grid collapsed more than twelve times. A country with proven gas reserves of 209 trillion cubic feet cannot reliably power itself. The state refineries that consumed $18–25 billion in maintenance expenditure remain offline. The currency trades at multiple rates depending on access. Security concerns—Boko Haram in the northeast, kidnapping in the northwest, pipeline vandalism in the delta—add friction to every transaction.

This is not bad governance in the sense of malice. It is governance where discretion dominates rules, where coordination costs exceed benefits, and where the state has become a venue for allocation rather than a platform for production.

The consequence for capital is predictable: tenor shortens, returns demanded rise, and capital becomes extractive rather than compounding. Nigeria is not "uninvestable." It is mispriced by optimists and overpriced by cynics—unless you structure properly.

What Reverses Regression

Regression ends when elites conclude—through pain or political evolution—that order pays more than disorder.

Ghana offers a partial example. After defaulting in 2022 and completing a domestic debt exchange in 2023, Ghana finalised its Eurobond restructuring in October 2024 with 98 per cent bondholder participation. The nominal value of external debt was reduced by $5 billion, generating $4.3 billion in debt service savings during the IMF programme period. This is not recovery—Ghana's fiscal space remains constrained, and the IMF programme continues until May 2026—but it is stabilisation through enforced discipline.

The uncomfortable conclusion: until incentives change, reform is cosmetic. And until reform is structural, capital will treat the country as a trading venue, not a compounding destination.

This is Part 4 of a 10-part series on African investment, state capacity, and capital allocation.

Previous: ← Part 3: Africa's Trajectory Winners

Next: Part 5: Return-on-Risk →