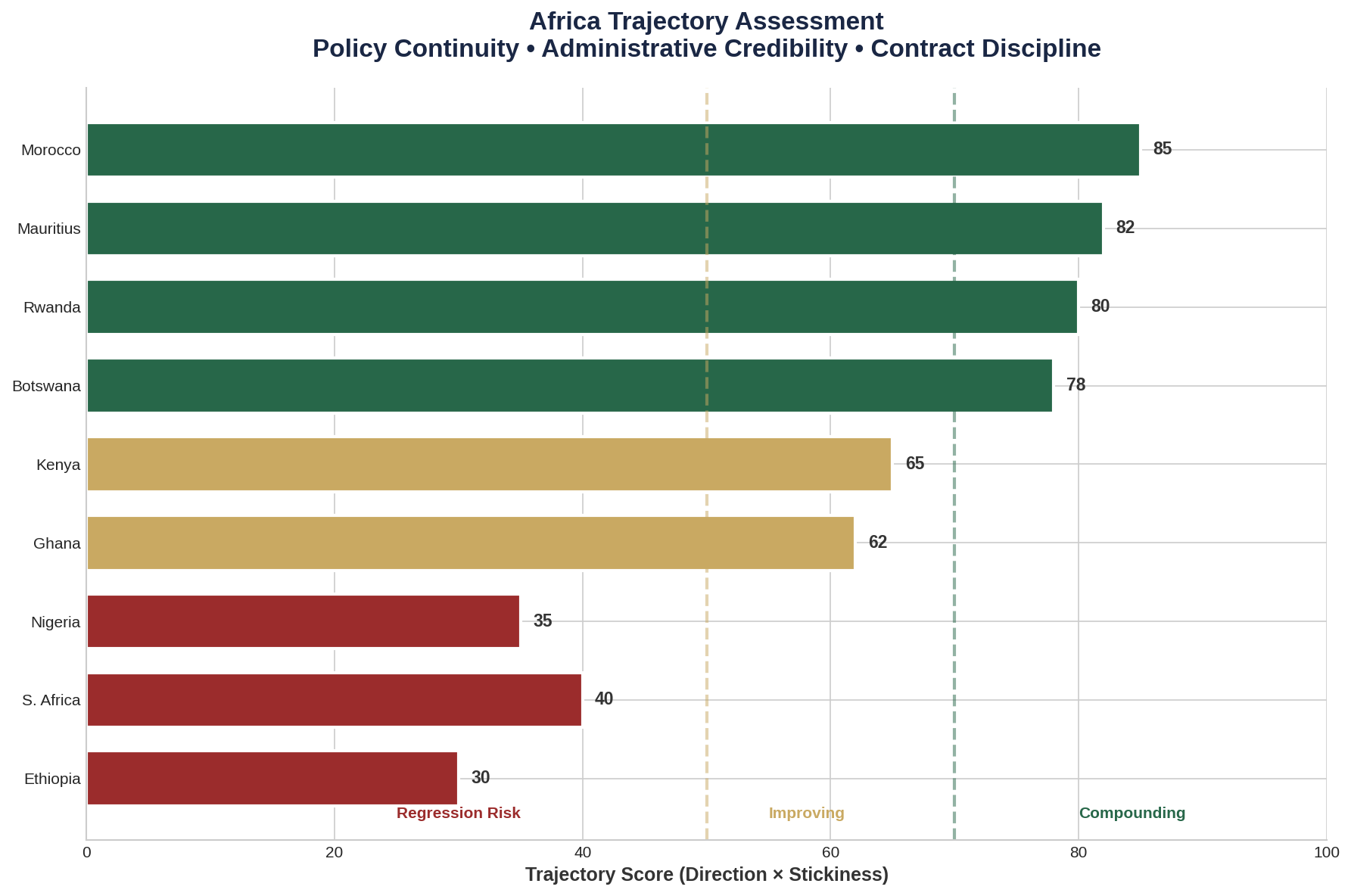

Trajectory is not a mood. It is a production system that shows up in three places: policy continuity, administrative credibility, and contract discipline.

Trajectory is direction multiplied by stickiness—how hard it is to reverse progress. A country can have a "good year." Trajectory asks whether the next ten years are structurally more likely to improve.

Africa trajectory assessment: The compounding band versus regression risk countries.

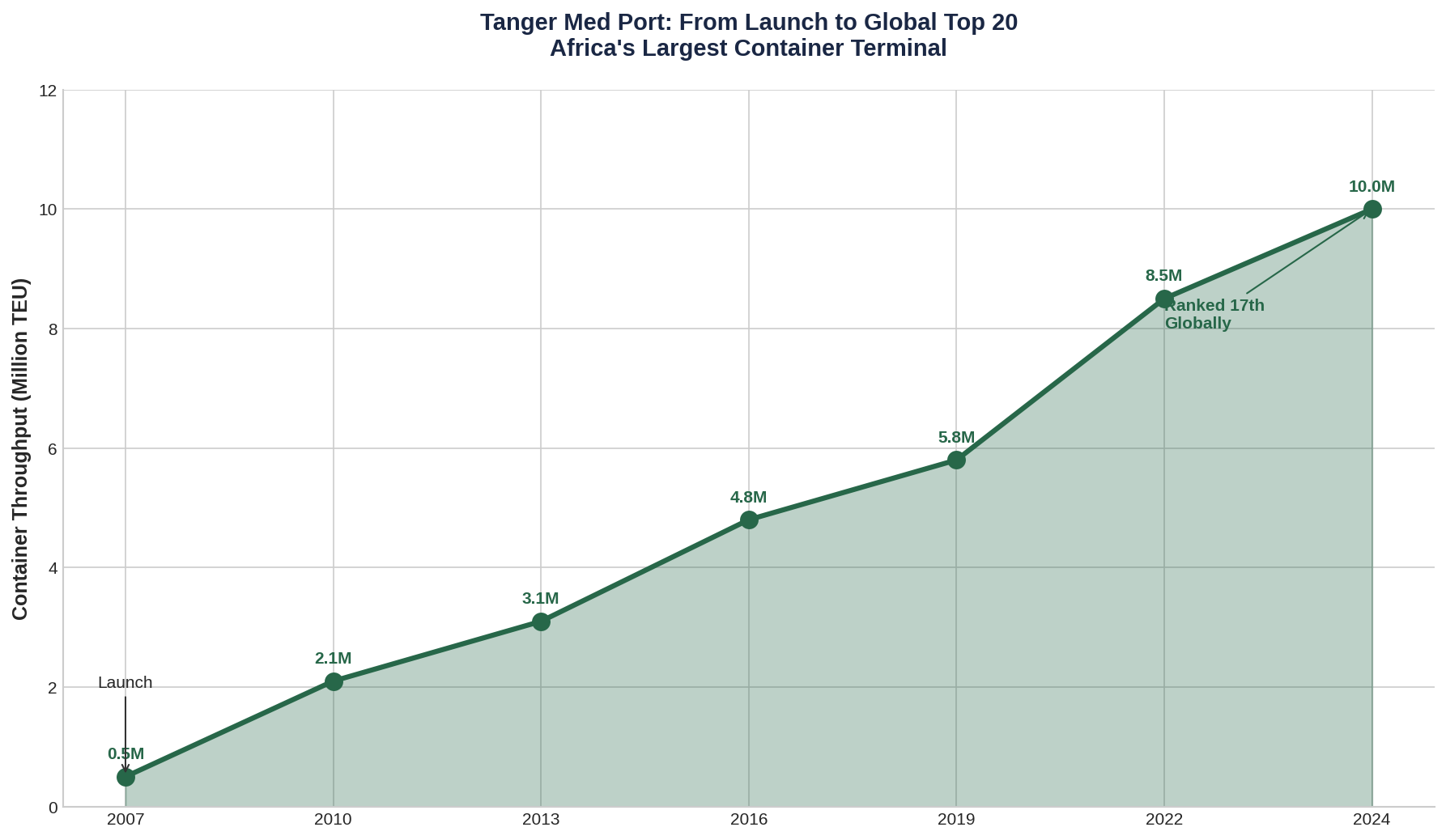

Morocco: The Tanger Med Model

Morocco offers the clearest example of trajectory thinking translated into infrastructure reality. The Tanger Med port complex, launched in 2007, has become the Mediterranean's leading container terminal and Africa's largest. In 2024, it handled approximately 10 million twenty-foot equivalent units—an 18.8 per cent increase year-on-year—and ranked seventeenth globally in container throughput, entering the top twenty for the first time.

Tanger Med's rise from launch to global top 20—a trajectory of execution, not announcements.

More instructive than the statistics is the development model. Since launch, Tanger Med has attracted cumulative investments exceeding $13 billion, split between public infrastructure and private industrial zones. The port complex now spans 3,000 hectares, connects to over 180 ports worldwide, and is powered entirely by renewable energy. The industrial zones host 1,400 companies employing 130,000 workers across automotive, aeronautics, textiles, and renewable energy—including Africa's second-largest automobile production base.

The Morocco Model

Build world-class logistics infrastructure → Connect to global value chains → Treat credibility as a compounding asset → Attract commercial (not concessional) capital.

In November 2024, the International Finance Corporation and MIGA partnered with Tanger Med on a $500 million expansion of the truck terminal—the first sustainability-linked loan in Morocco's port sector. This was not concessional development finance. It was commercial capital, priced competitively, because the underlying asset had demonstrated execution.

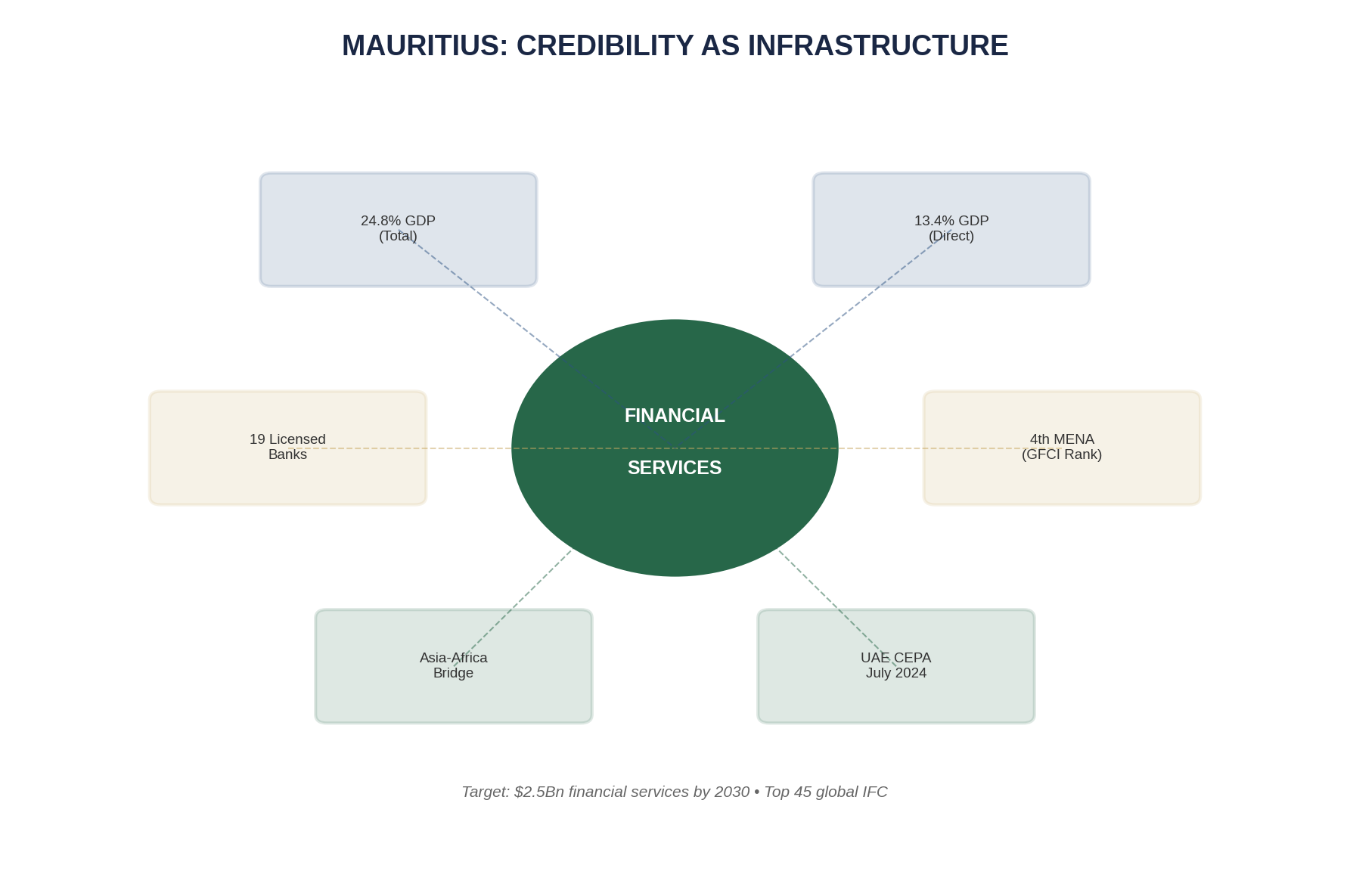

Mauritius: Credibility as Export

Mauritius has built institutional credibility as exportable infrastructure.

Mauritius is a different archetype: a small island economy that has systematically built institutional credibility as exportable infrastructure.

The financial services sector contributed 13.4 per cent of GDP in 2024 directly, and 24.8 per cent including indirect effects. Mauritius has Africa's highest level of financial inclusion. In the Global Financial Centres Index, it ranks fourth in the Middle East and Africa region—behind Dubai, Abu Dhabi, and Casablanca—and was identified as sixth globally among centres expected to grow in prominence.

What makes Mauritius investable is not size but predictability. Nineteen licensed banks, a well-developed regulatory framework, and deliberate positioning as the bridge between Asian capital and African opportunity. In July 2024, Mauritius signed a Comprehensive Economic Partnership Agreement with the UAE—the first between the Emirates and an African country—targeting fintech, healthcare, and tourism investment.

The strategic target is explicit: increase financial services gross value from $1.7 billion in 2024 to $2.5 billion by 2030, and reach forty-fifth place in global financial centre rankings. This is not aspiration—it is a measurable business plan for a sovereign.

Rwanda: Execution Stickiness

Rwanda's trajectory is built on enforced discipline and institutional memory. The government completed Phase 1 of its Urban Development Project in February 2024, delivering infrastructure improvements across six secondary cities. A $1 billion framework agreement with South Korea was signed in 2024, replacing a previous $500 million commitment. Kigali Innovation City broke ground in September 2024, with Africa50 as implementation partner, targeting $2 billion in value and 50,000 jobs at completion.

The pattern is execution stickiness. The ICT sector now accounts for 17 per cent of exports. The Open Contracting Data Portal creates accountability infrastructure. The government's stated objective—middle-income status by 2035, high-income by 2050—is backed by measurable interim milestones.

Critics point to political constraints on opposition and media. These are legitimate concerns that create long-term legitimacy risk. But for capital, the question is narrower: does the state deliver on what it commits? Rwanda's answer, measured empirically, is yes more often than most.

Why Winners Can Still Fail

Trajectory is probability, not destiny. Three failure modes recur even in compounding states:

Legitimacy Debt: A tightly managed system can compound quickly—until a legitimacy shock arrives. When political inclusion lags economic ambition, stability becomes fragile.

External Dependence: Small open economies are vulnerable to tourism cycles, commodity terms-of-trade swings, and external financing conditions. A state can be well-run and still get hit.

Complacency as Policy: Success breeds institutional arrogance. When the bureaucracy starts believing its own myths, reform slows and the edge dulls.

The lesson for investors: stop asking "Who is growing?" Start asking: Who can enforce? Who can pay? Who can resist populist sabotage? Who can keep a policy promise longer than one budget cycle?

Sources

- IFC-MIGA Tanger Med Partnership

- Mauritius Investment Climate - US State Department

- Rwanda Urban Development Project - Ministry of Infrastructure

This is Part 3 of a 10-part series on African investment, state capacity, and capital allocation.

Previous: ← Part 2: State Capacity